Page 95 - claims information pack ebook_e

P. 95

Guidelines for presenting claims in the tourism sector

7.2.9 A claim for property damage should simply your calculations even though they may be

describe the damage caused and show the for different periods. For example you may be

cost of reasonable repair or replacement. claiming for a period of three months that spans

Please note that in the case of replacement two different financial years. In this case official

you should state when the original equipment documents covering each year and the three

was purchased and show a calculation to years prior to the incident will be required. Where

demonstrate the deduction of fair wear and computerised records of revenue and/or costs

tear. are maintained within the business, these should

be provided in as much detail as possible for the

7.2.10 When submitting your claim you should claim period and for two or three comparable

provide accounts for the last three years, periods from previous years, where available.

where available. Even if you do not need to Where computerised records are not available,

produce official accounts to the authorities, revenue losses may be established through

you should include any business records the submission of: reservation/booking sheets,

that you may have. Where official accounts restaurant or letting diaries, logbooks or any other

or statements of return are required for available information. These should be provided

18

the business for legal or tax reasons, together with bank statements and/or cash

these should be provided in support of receipt books for the business.

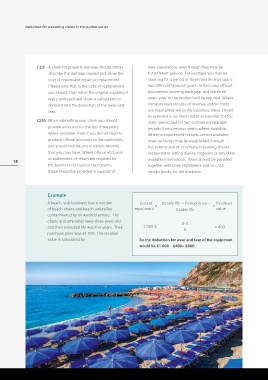

Example

A beach-side business has a number Cost of Usable life – Period in use = Residual

X

of beach chairs and beach umbrellas equipment Usable life value

contaminated by oil washed ashore. The

chairs and umbrellas were three years old 5-3

and their expected life was five years. Their 1 000 X 5 = 400

purchase price was £1 000. The residual

value is calculated by So the deduction for wear and tear of the equipment

would be £1 000 - £400= £600.